The real cost of car theft and accidents

July 11, 2019

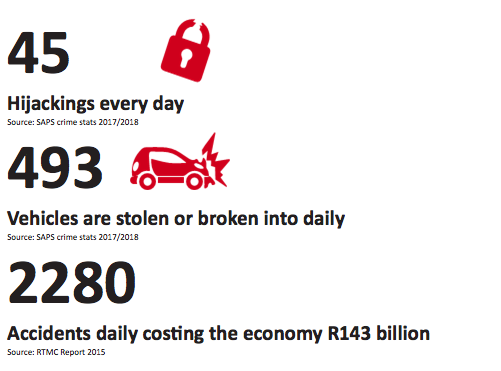

While insurance is an essential aspect of recovering financially from a vehicle theft or accident, there are still unexpected costs you may not have planned for, and some which you cannot attach a monetary value to.

“The best advice is to mitigate your risk as far as possible with correctly scoped insurance and advice, deploy security measures to deter would-be criminals, to strictly adhere to road safety rules and drive defensively,” says Mandy Barrett, of insurance brokerage and risk advisors, Aon South Africa.

Consider the unexpected costs and how to mitigate them:

- Insurance deductible or excess – an insurance claim is subject to a basic excess, usually 5% of the loss. If you are over the age of 55 years, you don’t pay a basic excess on Aon designed personal products.

- Your monthly insurance premiums could increase following a claim due to the loss of your ‘no claim bonus’.

- Mitigate against theft – park in a safe area and lock up at night. Most insurers will offer a premium discount should you volunteer to install an approved tracking system where the policy condition does not require one.

- Check that you have included the maximum car hire on your policy to avoid the cost and inconvenience of being without transport.

- Avoid leaving valuables in your vehicle – if unavoidable, make sure they’re out of sight. Valuables must normally be specified under All risks or they won’t be covered.

- Car remote jamming remains a trend and there is generally no cover if there is no evidence of break-in to your vehicle – it is important to check that your car is locked before walking away. Speak to Aon about our All Risks cover on your personal insurance.

- Understand the Basis of Loss Settlement on your insurance – Retail value is the price at which the dealer will sell a vehicle to you. Market value is what you could expect if you trade the vehicle in. Insurers will usually stipulate on which basis the claim will be calculated.

- Credit shortfall cover should be taken where the outstanding balance exceeds the retail value of the vehicle, enabling you to settle outstanding debt if your car is stolen or written off in an accident.

- Drive Defensively – maintain awareness of road and weather conditions, other road users and hazardous situations and take steps to prevent becoming the cause of or involved in an accident.

- It is the responsibility of the driver to take due care and abide by the rules of the road and keep your vehicle in a roadworthy condition. Weigh up the real costs of claiming for an event that could have been avoided in the first place. It all forms part of the required reasonable measures that insurers ask of you to prevent loss.

“Your ultimate goal is to mitigate your risk as far as possible and have appropriate insurance in place for those mishaps that cannot be avoided, putting you back in the same position financially as you were before the loss,” explains Mandy.

“This is where the value of having an expert broker by your side comes to the fore. Your expert broker will guide you through understanding the policy wording, and they will also point out any gaps in your insurance cover that could leave you compromised – something many people only discover at claims stage when it’s too late and they’re out of pocket,” Mandy concludes.